Over the past 10 years, China's bond market embraced the world with broader and more convenient channels for investors and bond issuers to benefit from the development dividends of the Chinese economy.

From widening access and lowering threshold to simplifying procedure requirements, a host of investment channel expansion and facilitation measures were taken to accelerate the paces of opening up of the bond market.

-- Broader opening up attracts diversified global participants

On expanding inbound investment channels, China allowed in March and May 2013 qualified foreign institutional investors (QFIIs) and Renminbi qualified foreign institutional investors (RQFIIs) to invest in the interbank bond market.

In February 2016, more types of overseas financial institutions such as commercial banks, insurers, securities companies, and fund firms were permitted to enter the interbank bond market and conduct transactions such as cash bond trading.

In July 2017, northbound trading of Bond Connect, a mutual market access scheme allowing investors from the Chinese mainland and Hong Kong Special Administrative Region (HKSAR) to invest in each other's bond market, commenced, offering a new channel for overseas small and medium-sized institutional investors to enter China's bond market.

Through the opening up moves, China's bond market has been one safe haven for global financial market players and RMB-denominated bonds have also been favored as an emerging asset type.

On introduction of overseas issuers, more financing channels for a wider range of overseas issuers are available in the past decade.

For instance, Daimler issued in 2014 landmark corporate panda bonds in China, marking the resumption of panda bonds issuance after a long hiatus in China. In December 2015, pilot panda bond issuance for enterprises from the HKSAR kicked off on China's exchange bond market. In March 2018, Shanghai and Shenzhen stock exchanges issued circulars on pilot Belt and Road bonds, encouraging government institutions, companies, and financial institutions from the Belt and Road Initiative countries and regions to issue panda bonds. In September 2018, China promulgated rules to regulate panda bond issuance on interbank bond market by overseas issuers of multiple types.

Industry experts said that with rapid growths in recent years, panda bonds have become an effective means to facilitate cross-border investment and financing of overseas issuers.

-- More choices of investment products for global investors

On boosting bond issuance in Hong Kong, China allowed in May 2012 qualified non-financial institutions from the Chinese mainland to issue RMB-denominated bonds in HKSAR, injecting new impetus into the primary bond market there.

In December 2021, Chinese regulators abolished the interim rules for bond issuance in HKSAR by financial institutions from the Chinese mainland, which simplified related record filing and other procedures and was expected to greatly boost bond issuance in HKSAR's bond market.

Moreover, the anticipated quicker bond issuance will further enrich the RMB-denominated investment products in HKSAR and expand the channels of usage for overseas RMB, said a HKSAR-located bank trader, adding that these will be good for drawing more overseas enterprises and financial institutions to put RMB into their baskets of reserve assets.

Besides, southbound trading under Bond Connect kicked off in September 2021, providing a convenient channel for Chinese mainland institutional investors to invest in offshore bonds via Hong Kong bond market.

With northbound and southbound trading both in operation, the two-way opening up of China's bond market will contribute to improving the global acceptance of RMB and speeding up the internationalization of RMB, held analysts.

-- Attractiveness of RMB bond assets intensified

Resulting from the opening-up moves, China's bond market has seen gradual inclusions of government bonds into the three global mainstream bond indexes since 2019, reflecting global investors' confidence in the long-term development prospects of Chinese economy and broader financial market opening-up.

Chart I: Details about inclusion of Chinese government bonds into three global benchmark bond indexes

| Indexes | Date of formal inclusion | Type of bonds included | Term of inclusion | Weighting | Projected capital to be attracted | Progression |

| Bloomberg Barclays Global Aggregate Index (BGAI) | April 1, 2019 | RMB-denominated China's Treasury bonds and policy bank bonds | 20 months | About 6% | USD150-200 bln | Completed |

| J.P. Morgan's Government Bond Index-Emerging Markets (GBI-EM) indices | Feb. 28, 2020 | RMB-denominated Chinese government bonds | 10 months | - | USD20 bln | Completed |

| FTSE World Government Bond Index (WGBI) | Oct. 29, 2021 | RMB-denominated Chinese government bonds | 36 months | 5.25% upon completion, up to flexible adjustment | USD150-260 | To be completed by Oct., 202 |

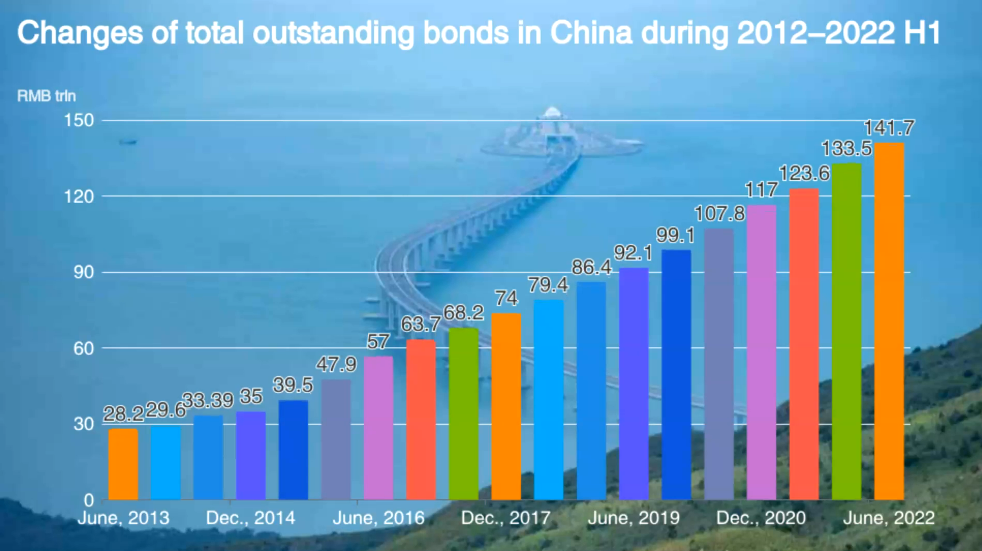

Statistics with the People's Bank of China (PBOC), the Chinese central bank, showed that by the end of June 2022, China's bond market had grown from the world's third largest one to the second largest, with aggregate outstanding bonds at 141.7 trillion yuan, more diversified products and greater favor from global investors in recent years.

Chart II: Changes of total outstanding bonds in China during 2012-2022 H1

Data source: PBOC

By June this year, bond holdings by overseas institutional investors increased all the way from 436.776 billion yuan in June 2014 to 3.289 trillion yuan, according to data with China Central Depository & Clearing Co., Ltd.

In the first half of 2022, however, overseas investors slightly reduced their bond holdings because of the higher 10-year U.S. T-bond yield thanks to the U.S. Fed's balance sheet reduction and interest rate hiking and the weaker Chinese currency as well.

But currently, the yield spread between the 10-year T-bonds of China and the United States stands still at relatively high levels in terms of real interest rate and due to the high inflation in the United States.

Generally, China's bond products boast advantages in bringing investors relatively stable returns and compared with developed economies and part of the emerging economies, overseas investors' bond holdings in China are not high by proportion.

As a sound vehicle for global investors to diversify portfolios, RMB-denominated bonds are expected to attract more mid- and long-term investment into China's bond market in the future, analysts said.